A major worry for potential bankruptcy clients who own their home is whether it could be lost in a bankruptcy filing. It is important to realize that losing a home or other significant property in Wisconsin is rare due to its debtor-friendly bankruptcy laws, but the equity in your house (total value subtracted by total liabilities) determines whether the home is 100% protected.

How did we get here?

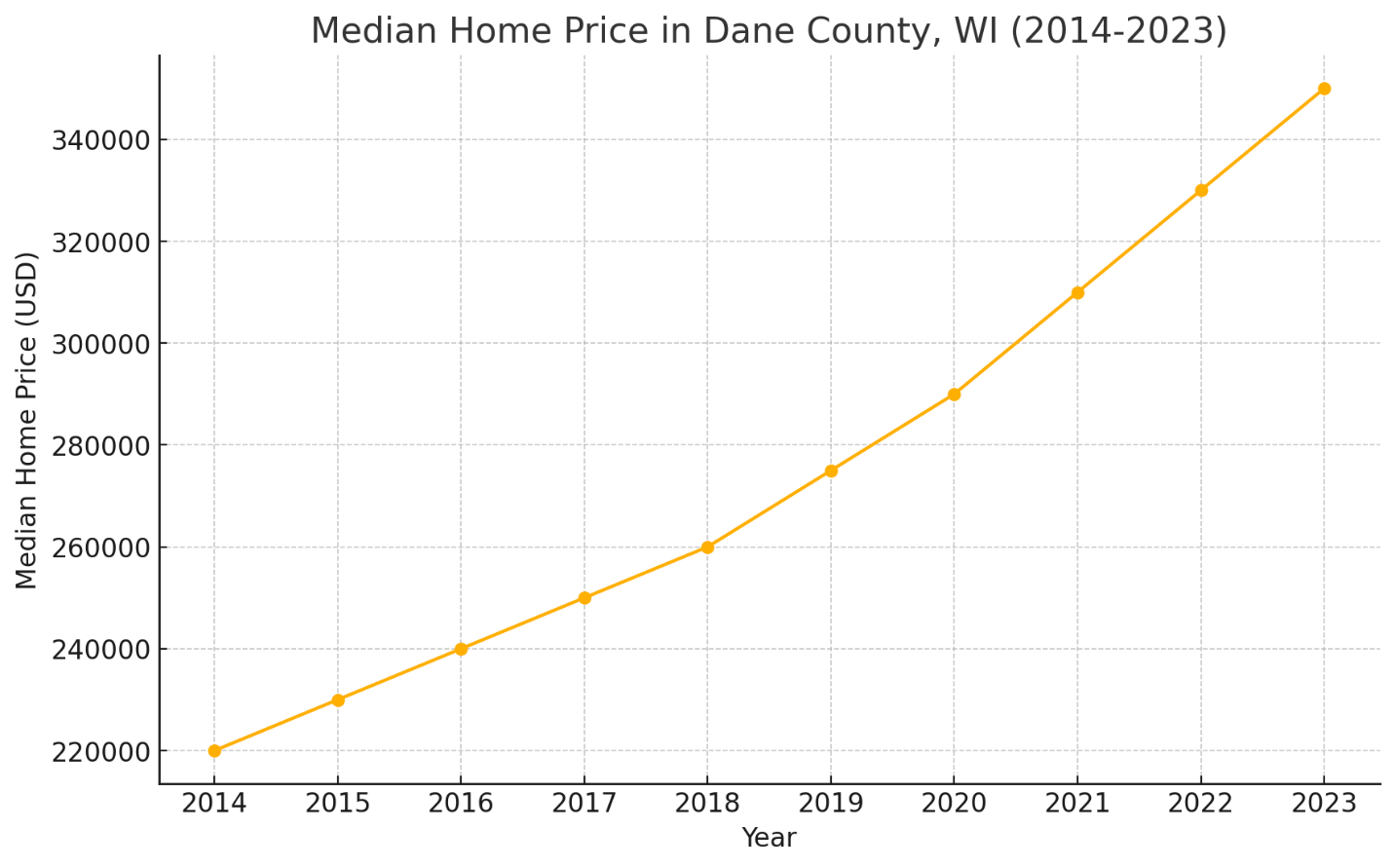

Wisconsin has seen rapidly increasing home prices over the past decade. https://www.wra.org/Resources/Property/Wisconsin_Housing_Statistics/ Home values have particularly increased in larger urban areas with the rise and popularity of work-from-home, urban population growth, and a limited inventory of new housing available in such areas. Dane County, particularly Madison, has experienced steep increases in median prices over the past decade:

What to do?

Where do increased home values leave Wisconsin homeowners? How can you protect your primary residence AND eliminate other debts through bankruptcy? Chapter 7 bankruptcy is designed to provide a fresh financial start by liquidating your unprotected assets to pay off creditors, but when is a home protected and when it is vulnerable? Bankruptcy pros and attorneys Jenna ER Morrison and Brent Berning share 30 years of their combined wisdom below.

Step 1. VALUATION. The value of your home is what a willing buyer would pay for it in the real world. To determine your home value, the Trustee appointed to your bankruptcy will probably look at the real estate tax bill first, but those valuations tend to be lower than the actual market value as prices have increased faster than the county assessors’ tax-assessment valuations. You could pay for an appraisal, but those are expensive. A cost-effective alternative might be to have a realtor or other professional do a Comparative Market Analysis (“CMA”) on the home. Or you, with the help of your bankruptcy attorney, could look to Zillow, Redfin or a similar site to obtain records for recent neighborhood sales of comparable properties, making sure to account for any needed repairs that impact sale value. Remember, bankruptcy is a rare time in life when it is to your advantage to have limited assets! The lower the valuation, the greater the chance you qualify for a fresh start without losing assets.

Step 2. LIABILITIES. With the help of your bankruptcy attorney, you will want to produce documentation of the current balances for all mortgages, home equity lines of credit, or other liens against your house. Don’t forget to include debts like windows or other improvement home loans that may be liens as well. You may wish to do a title search on the property to confirm the above. Child support and tax liens are also liens against a home that can be overlooked.

Step 3. Know Your Exemptions (Homestead): With Wisconsin’s generous homestead exemption, bankruptcy filers can protect up to $75,000 ($150,000 per married couple) of equity in a homestead. “Equity” is the net profit after a hypothetical sale of your home subtracting mortgages, closing costs, realtor fees, and other liens that would have to be paid. We typically recommend using an 8% “cost of sale.”

For example, if your home’s market value is $500,000 with a $200,000 first mortgage balance and a $100,000 home equity line of credit, the bankruptcy petition would list:

$500,000 estimated fair market value

-$200,000 1st mortgage

-$100,000 2nd mortgage

-$40,000 cost of sale=$160,000.

Step 4. Avoid Non-Exempt Equity: If your home equity exceeds the exemption limit, there’s a risk that the Trustee might try to sell the property to pay creditors or ask you for the amount that could be cleared in a hypothetical sale. In the example above, if you are a married couple filing together, the non-exempt equity is $10,000 ($160k – $150k exemption). A Trustee would be looking to recover $10,000 in a Chapter 7 bankruptcy from you.

I have Non-Exempt Equity, now what?

Step 5. Generally speaking, a Chapter 7 Trustee does not want to sell your home. It is significant work, but they receive a percentage of assets sold and a Trustee is hired to seek non-exempt assets to sell and pay your debts.

Options:

- Negotiate with the Trustee to buyout the non-exempt equity. In the example above, you could offer to pay the Trustee $10,000. This strategy will only work if you have access to funds, such as in a bank or a retirement account.

- Argue No Assets for Creditors: Under the Bankruptcy Code, the recovery of assets is meant to benefit creditors, not Trustees. In many cases a Trustee would not be able to pay a significant amount toward your debts if the house were sold. The Trustee fees range 5-25% of the amount of non-exempt equity and an attorney (often the same Trustee) also gets paid an hourly fee of several hundred dollars per hour to represent the Trustee in the asset recovery process, so it is very possible that if the Trustee were to sell your home there would be very little leftover to pay any creditors. Continuing the example above, if the Trustee recovers $10,000 and the Trustee’s fee would be 25% of the first $5,000 disbursed and 10% of the next $5,000 for a total of $1250+$500=$1750. If the lawyer appointed to represent the Trustee is paid for 10 hours of work at $350/hour that equals $3500. So there would only be $10,000 -$2750-$3500= $3750 of the $10,000 to pay to unsecured creditors. You could ask the Court not to disallow a sale.

- Do you have any judgment liens (state court judgments)? By operation of state law a judgment lien attaches to non-exempt equity in your home. Since your bankruptcy doesn’t discharge for several months after filing, you could argue that judgment liens encumber the equity in the property and so there would be no reason for the Trustee to sell the property. The counter-argument is that the bankruptcy avoids the liens. However, those liens will continue to show on state lien searches after a federal bankruptcy case is complete and would need to be satisfied (or cleared) in order to sell the home.

- Does your home require repairs? A leaky roof, plumbing issues, etc? Invite the Trustee to the house or take pictures demonstrating the state of disrepair. Obtain estimates of what it would cost to repair the property.

Step 6. Consider Alternatives: If you have non-exempt equity, you may choose to file the Chapter 7 and rely on the fallback of a Chapter 13. If the Chapter 7 Trustee threatens to sell the home, you might be able to convert to Chapter 13 to stop them from doing this. While there is no “absolute right” of conversion from Chapter 7 to Chapter 13, typically courts favor conversion in these situations for the “honest, but unfortunate debtor.”

If protecting your home is a top priority, filing your case as Chapter 13 bankruptcy may be the best choice. Chapter 13 bankruptcy allows you to restructure your debts and keep your assets, including your home, under a court-approved repayment plan that pays at least as much to unsecured creditors as they would receive in a Chapter 7 bankruptcy.

Continuing the example above, in a Chapter 13 Plan, as long as you would pay at least $10,000 to unsecured creditors over the life of the plan (typically 3-5 years), you would be able to keep your home.

Another risky-“ish” strategy would be to look at converting non-exempt equity to protected assets, but you should consider this option with caution and the advice of legal counsel. Too much pre-bankruptcy planning can result in denial of discharge, loss of assets, or even sanctions, fines, or other adverse consequences.

Navigating asset protection in bankruptcy requires careful consideration of Wisconsin-specific valuation and exemption rules. By understanding how these valuations and exemptions work, consulting with legal professionals, and being proactive, you can protect your home and move toward a more stable financial future. Remember, every situation is unique, so personalized legal advice is essential to make the best decisions for your circumstances.

About the Authors:

Attorney Jenna Morrison owns the law firm Badger Bankruptcy LLC in Madison, WI. She was born in Madison and graduated from the University of Iowa Law School. She is now practicing primarily in the areas of consumer bankruptcy and debt relief. Jen is married to her husband, Mark, and has three sons. She enjoys reading, walking, and being with her family in her free time. You can find out more about Jenna Morrison at www.badgerbankruptcy.com.

Attorney Brent Berning owns his law practice in Milwaukee, Wisconsin – Berning Law, LLC. He has been helping people get out of debt for over 16 years. He grew up near Madison and lives in Milwaukee with his wife and 18-month-old daughter. You can find out more about attorney Brent Berning at www.milwaukeebankruptcylaw.com.